Stop-Loss Sizing: Sizing Crypto Futures Positions with Funding Rate Drag

Learn how perpetual futures funding rates create position drag and discover how to adjust your stop-loss and trade sizing to manage risk.

Stop-Loss Sizing: Crypto Futures Funding Rate Drag

Trading cryptocurrency perpetual futures contracts allows investors to take leveraged long or short positions without dealing with expiration dates. However, perpetual futures carry a unique risk element: Funding Rates. Funding rates are periodic payments exchanged between buyers (longs) and sellers (shorts) to anchor the futures price to the underlying spot price.

If you hold a leveraged position open for days or weeks, funding payments create a persistent position drag that can degrade your margins, bringing your liquidation price closer and invalidating your technical stop-loss.

In this guide, we will analyze funding rate mechanics, map the payment flows, and adjust position sizing to manage drag risk.

🧐 How Perpetual Funding Rates Work

Perpetual contracts have no delivery date, meaning they could drift away from the spot market price indefinitely. To prevent this, exchanges calculate a funding fee every 8 hours (or hourly on some platforms):

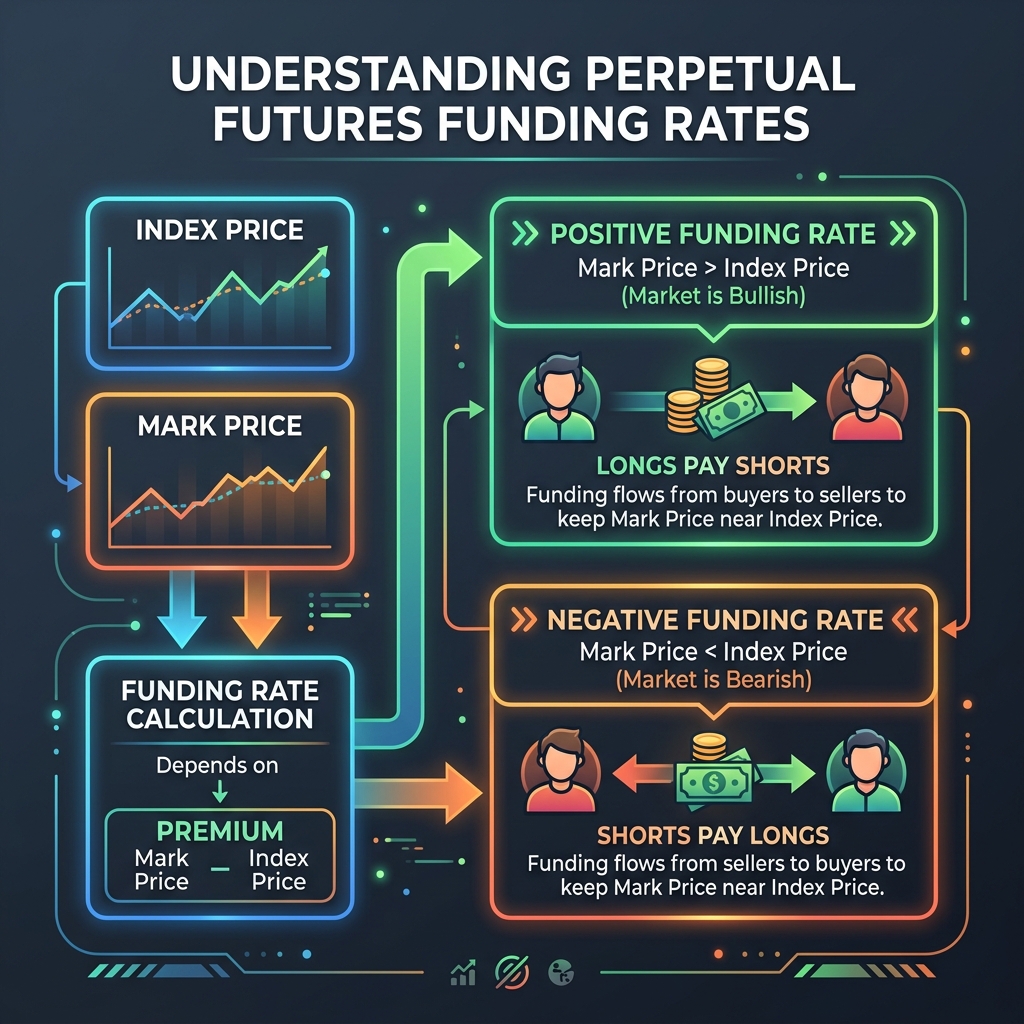

- Mark Price: The active price of the perpetual futures contract.

- Index Price: The average spot price of the asset across multiple exchanges.

When the Mark Price is higher than the Index Price, the funding rate is positive. Longs pay Shorts. When the Mark Price is lower than the Index Price, the funding rate is negative. Shorts pay Longs.

📊 Perpetual Funding Payment Flow

Below is a visual outline of how the relation between Mark and Index prices dictates funding flow:

📉 The Funding Rate Drag Calculation

Let's look at the mathematical impact of a positive funding rate on a leveraged long position. * Account Balance: $10,000 * Position Size: $100,000 (10x leverage) * Average Funding Rate: 0.05% per 8 hours (0.15% per day)

$$\text{Daily Funding Payment} = \$100,000 \times 0.0015 = \$150 \text{ per day}$$

If you hold this position open for 10 days, you pay $1,500 in funding fees alone—representing 15% of your collateral account equity! This fee is deducted directly from your margin account, moving your liquidation price closer to your entry.

🛠️ Adjusting Your Sizing and Stop-Loss for Funding Drag

To prevent funding rate drag from triggering premature liquidations:

- De-leverage: If funding rates are extremely positive (which is common during bullish market peaks), reduce your leverage. This reduces the size of your position relative to your margin, decreasing your daily funding fee.

- Incorporate Drag into Stop-Loss Distance: When calculating your technical stop-loss using a Position Size Calculator, deduct your estimated funding payments from your risk budget first.

- (Read our guide on Position Sizing for Leveraged Futures or review Spot vs Margin Risk Sizing to learn more about margin maintenance limits).

To measure volatility limits before setting stops, check out our Average True Range Stop Guide or compute swing boundaries using the Fibonacci Retracement Grid.

Join the Urbandigistore Hub

Subscribe to receive premium developer cheat sheets, advanced conversion techniques, and campaign optimization checklists. Zero spam, unsubscribe anytime.