Stop-Loss Sizing: Position Sizing with Average True Range (ATR) Multipliers

Learn how to select the optimal Average True Range (ATR) multiplier stop-loss distance based on your trading style, time horizon, and hold period.

Stop-Loss Sizing: Position Sizing with ATR Multipliers

Using the Average True Range (ATR) allows traders to calculate stop-loss levels that adjust dynamically to an asset's volatility. However, to execute this strategy, you must select an ATR Multiplier. If your multiplier is too tight, standard price noise will stop you out prematurely. If it is too wide, your risk distance increases, forcing you to buy fewer shares and reducing your capital efficiency.

In this guide, we'll explain how to choose the optimal ATR multiplier for your trading style and analyze stop boundaries.

📐 The Multiplier Risk Equation

To calculate your stop-loss level, the formula is:

$$\text{Stop-Loss Price} = \text{Entry Price} - (\text{ATR} \times M)$$

Where: * $M$: The volatility multiplier. * ATR: The current Average True Range (14) indicator value.

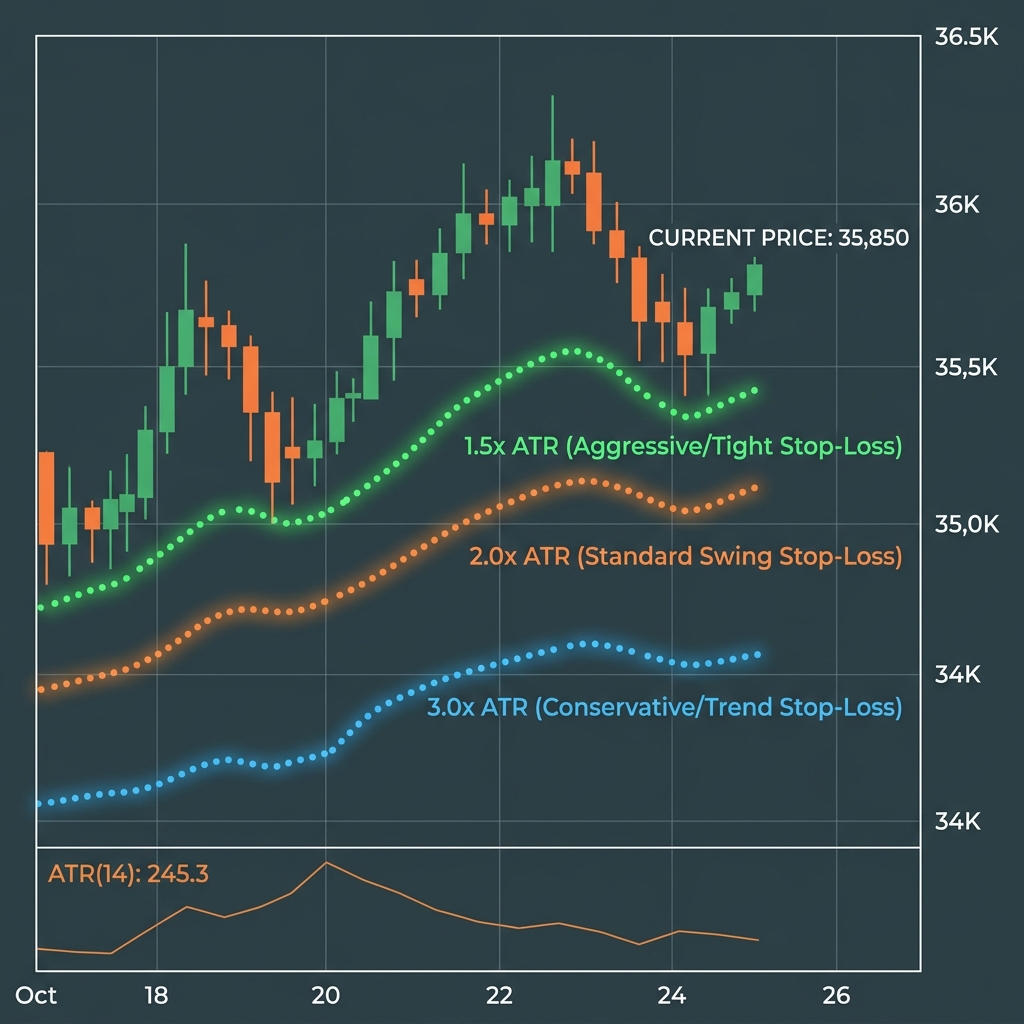

📊 Volatility Bands Comparison Infographic

Below is a technical layout illustrating price action bouncing inside three different ATR multiplier boundaries, helping you visualize noise-free zones:

🔍 Matching Multipliers to Your Hold Period

Selecting the correct value of $M$ depends on your trading time horizon:

1. 1.5x ATR (Aggressive / Tight Stops)

- Ideal for: Day traders and momentum scalpers.

- Characteristics: Minimizes stop distance, allowing for larger position sizes. However, it carries a high risk of getting stopped out by brief, noise-driven price spikes.

2. 2.0x ATR (Standard Swing Trading)

- Ideal for: Multi-day swing traders.

- Characteristics: The industry standard. Provides a comfortable buffer that allows the asset room to breathe through standard daily fluctuations while protecting equity.

3. 3.0x ATR (Conservative / Trend Following)

- Ideal for: Position traders, investors, and crypto trend-followers.

- Characteristics: Extremely resilient against fakeouts. Keeps you positioned through major trend expansions. Requires smaller position sizes due to the wide risk distance.

🛠️ Implementing ATR Stops

To implement these sizing models in your daily workflow: 1. Verify the current volatility index on your charts. 2. (See our ATR stop-loss calculations guide to review step-by-step math formulas). 3. Adjust for Leverage: If trading leveraged futures contracts, ensure your ATR stop sits well above your liquidation price. (Read Spot vs Margin Sizing Rules and Crypto Futures Leverage Sizing). 4. Calculate Positions Instantly: Use our browser-based Position Size Calculator to quickly model share counts and risk targets.

Join the Urbandigistore Hub

Subscribe to receive premium developer cheat sheets, advanced conversion techniques, and campaign optimization checklists. Zero spam, unsubscribe anytime.