Stop-Loss Sizing: Position Sizing with Risk-Adjusted Sharpe Ratio

Learn how to use the Sharpe Ratio to evaluate trading strategies and optimize portfolio allocations based on risk-adjusted performance.

🔧 Interactive Utility Tool

Try the free, 100% secure client-side tool associated with this guide. No registration required.

Position Sizing with Risk-Adjusted Sharpe Ratio

When constructing a multi-asset trading portfolio, simply allocating equal capital to every trade is sub-optimal. Some strategies have high win rates but experience large drawdowns, while others have steady, low-volatility equity curves. To optimize risk-adjusted returns, quantitative managers allocate capital based on performance metrics like the Sharpe Ratio.

In this guide, we'll explain the Sharpe Ratio formula, outline volatility normalization rules, and analyze trade allocations.

📐 The Sharpe Ratio Formula

The Sharpe Ratio evaluates the excess return of a strategy per unit of volatility:

$$\text{Sharpe Ratio} = \frac{R_p - R_f}{\sigma_p}$$

Where: * $R_p$: The expected return of the trading strategy. * $R_f$: The risk-free rate of return (e.g., U.S. Treasury yields). * $\sigma_p$: The standard deviation of the strategy's returns (a measure of volatility).

A strategy with a Sharpe Ratio above 1.0 is considered good, while ratios above 2.0 indicate exceptional risk-adjusted performance.

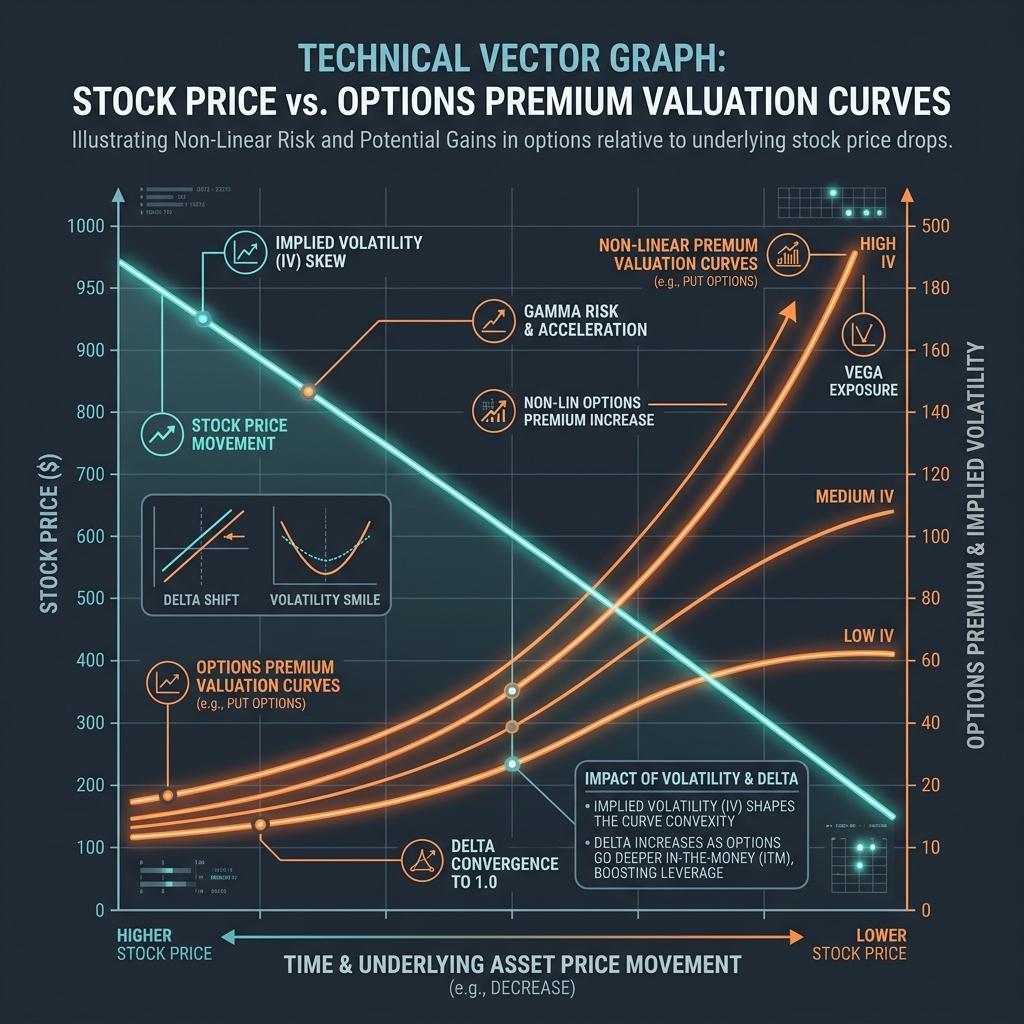

📊 Volatility Curves Reference

When trading options or volatile derivatives, risk exposure curves are non-linear. The chart below illustrates how option premium delta decay curves shift based on implied volatility (IV) and pricing boundaries:

🔍 Sharpe-Based Portfolio Allocation

To maximize portfolio stability, allocate capital proportionally to each strategy's Sharpe Ratio while scaling sizes inversely to their volatilities:

- Calculate Sharpe Ratios: Periodically review the monthly returns of each strategy.

- Risk-Weight Allocations: Assign larger capital weights to strategies that display high Sharpe ratios and low standard deviations ($\sigma_p$).

- Scale Down High-Variance Systems: Highly volatile trading systems must receive smaller capital allocations, ensuring they do not dominate the portfolio's total equity swings.

- (See our Kelly Criterion Sizing Guide to review mathematical formulas).

- Compute Positions Instantly: Use our browser-based Position Size Calculator to quickly model share counts and risk targets.

Join the Urbandigistore Hub

Subscribe to receive premium developer cheat sheets, advanced conversion techniques, and campaign optimization checklists. Zero spam, unsubscribe anytime.

🚀 Launch Interactive Tool

Ready to test this directly? Open the secure web tool in a new sandbox tab.