Stop-Loss Sizing: Position Sizing with Volatility-Adjusted ATR Percentage

Learn how to normalize the Average True Range (ATR) indicator across assets using ATR percentage to calculate risk.

Position Sizing with Volatility-Adjusted ATR Percentage

The Average True Range (ATR) is an excellent indicator for measuring market volatility. However, raw ATR is expressed in absolute price points. For example, a \$150 stock might have an ATR of \$3.00, while a \$60,000 cryptocurrency might have an ATR of \$1,200. Because raw values scale with the asset price, you cannot compare their volatilities directly.

To normalize volatility across different asset classes, professional traders use ATR Percentage (ATRP). In this guide, we'll explain the normalization formula, compare asset classes, and trace stop-loss boundaries.

📐 The ATR Percentage Formula

To calculate the volatility of an asset as a percentage of its current price, the formula is:

$$\text{ATRP} = \left( \frac{\text{ATR}}{\text{Current Price}} \right) \times 100$$

For example: * Asset A (Stock): Price = \$100, ATR = \$2.00. $$\text{ATRP} = \left(\frac{2}{100}\right) \times 100 = 2.0\%$$ * Asset B (Crypto): Price = \$50,000, ATR = \$1,500. $$\text{ATRP} = \left(\frac{1,500}{50,000}\right) \times 100 = 3.0\%$$

Even though Asset B's absolute ATR is much larger, its volatility-adjusted risk (3.0%) is only slightly higher than Asset A's (2.0%).

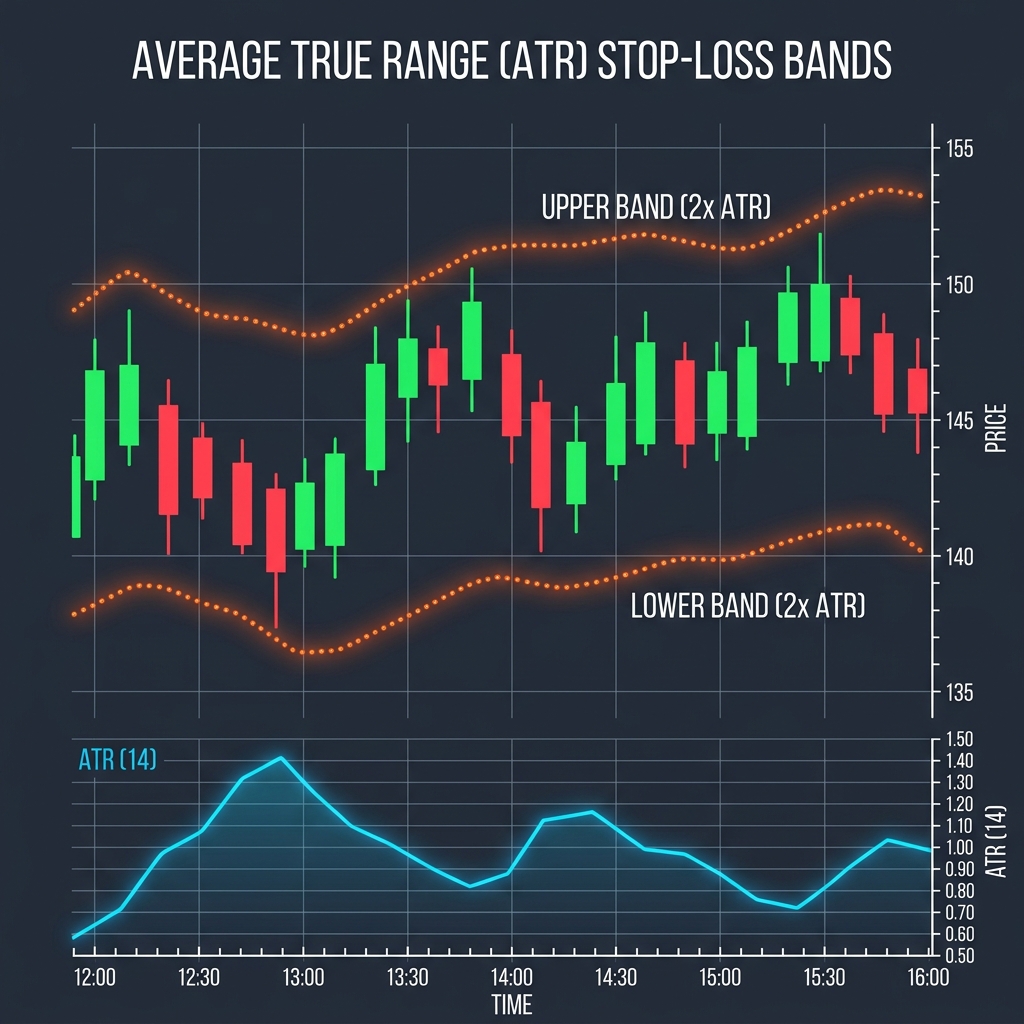

📊 Volatility Bands and ATR Visual Reference

Below is a technical layout illustrating price action and the corresponding ATR indicator bounds, which helps traders map their stop buffers:

🔍 Position Sizing with ATRP

Normalizing volatility allows you to standardize your risk exposure:

- Define Portfolio Risk: Limit your risk per trade to a fixed percentage of your account (e.g., 2%).

- Calculate ATRP Stop Distance: Choose an ATR multiplier $M$ (e.g., $2.0 \times \text{ATR}$). Calculate your stop distance as a percentage of entry price: $$\text{Stop Distance \%} = \text{ATRP} \times M$$

- Compute Share Count: Determine your position size using the percentage stop-loss buffer: $$\text{Position Size} = \frac{\text{Account Capital} \times \text{Risk \%}}{\text{Stop Distance \%}}$$

This method ensures that highly volatile assets automatically receive smaller position sizes, keeping your portfolio's total risk constant.

🛠️ Portfolio Sizing Utilities

To apply these risk formulas in your trading setups: * Choose Stop Multipliers: Read Choosing the Right ATR Multiplier Stop-Loss to select day vs. swing trade buffers. * Contrast Stop Types: Read ATR Stop-Loss vs. Fixed Percentage Stop-Loss to compare models. * Calculate Share Counts Instantly: Use our browser-based Position Size Calculator to quickly model share counts and risk targets.

Join the Urbandigistore Hub

Subscribe to receive premium developer cheat sheets, advanced conversion techniques, and campaign optimization checklists. Zero spam, unsubscribe anytime.