Stop-Loss Sizing: Sizing Stock Options Trades by Option Premium Volatility

Learn how Delta and Implied Volatility shape options pricing curves, and discover how to calculate volatility-adjusted stop-loss levels for options contracts.

Stop-Loss Sizing: Options Premium Volatility

When buying call or put options, many stock traders apply fixed stop-loss rules, such as "exit if the option premium drops 20%." However, stock options are derivatives whose price behavior is non-linear. Because of Implied Volatility (IV) shifts and time decay, option premiums do not move in a straight line relative to the underlying stock price.

In this guide, we'll explain how Option Greeks shape premium volatility and show you how to calculate volatility-adjusted stops.

📐 Understanding Option Greeks and Volatility

To size an options trade properly, you must evaluate three primary risk elements:

- Delta: Measures how much the option premium changes per $1.00 move in the underlying stock. A Delta of 0.50 means the premium moves $0.50 for every $1.00 swing in the stock.

- Gamma: Measures the rate of change of Delta. As the stock price moves, Delta shifts, creating a non-linear price curve.

- Implied Volatility (IV): Represents the market's expectation of future stock volatility. An increase in IV inflates the option premium, while a drop in IV (IV crush) deflates it, regardless of stock direction.

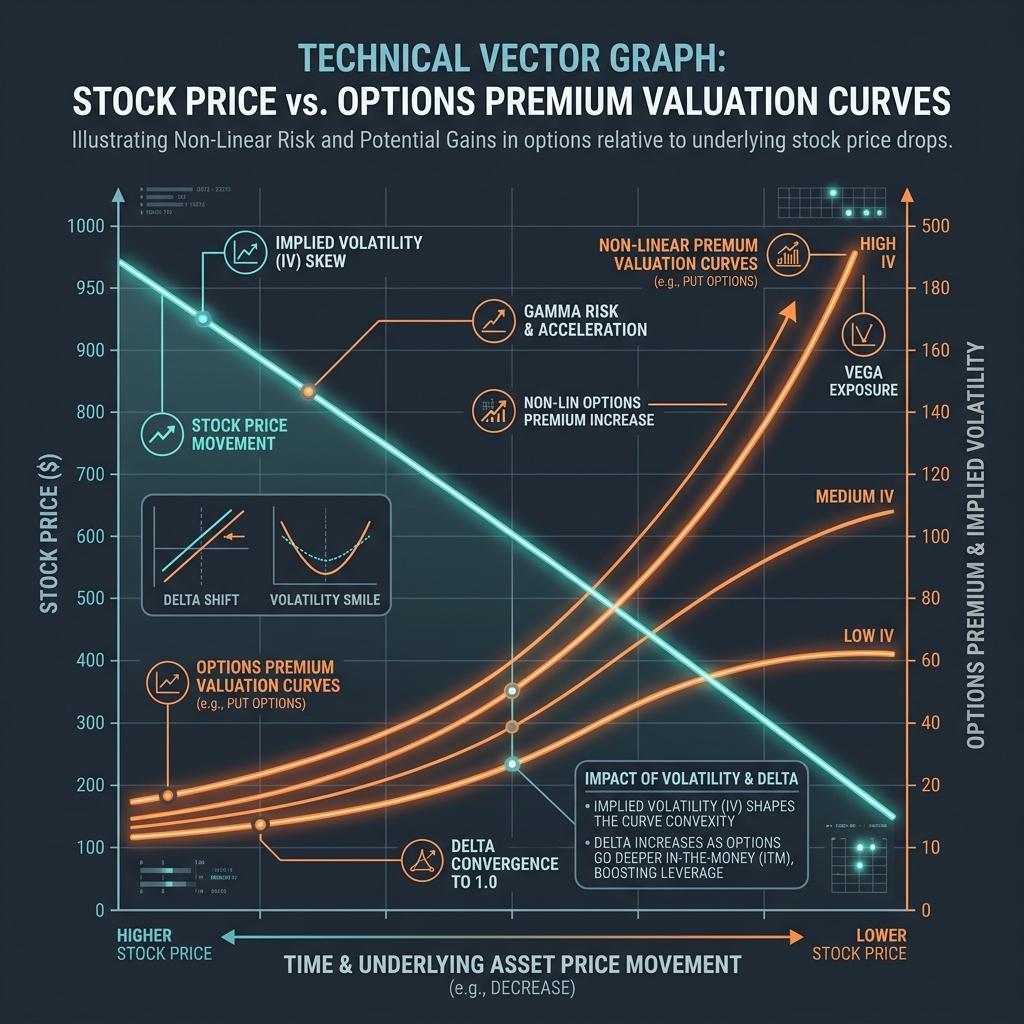

📊 Stock Price vs. Options Premium Valuation Curve

Below is a technical chart demonstrating how option premium curves behave non-linearly under different Implied Volatility (IV) scenarios compared to linear stock price drops:

🛠️ How to Size and Place Options Stops

To protect your margin capital without getting stopped out by standard option market noise:

- Stop the Stock, Not the Option: Define your technical stop-loss level on the underlying stock chart (e.g. Buy stock at $100, stop-loss at $95).

- Calculate Premium Value at Stock Stop: Use the option's Delta and Gamma to estimate what the contract will be worth if the stock hits your stop price ($95).

- Formulate Sizing: $$\text{Premium Stop Distance} = \text{Option Entry Price} - \text{Estimated Option Price at Stock Stop}$$ $$\text{Contracts to Buy} = \frac{\text{Account Cash Risk Budget}}{\text{Premium Stop Distance} \times 100}$$ (e.g., maximum risk is $200, premium stop distance is $0.50. Contracts = $200 / ($0.50 * 100) = 4 contracts).

By sizing this way, if the underlying stock hits your technical target ($95), your option contracts will be sold, and your total loss will align exactly with your target budget!

🚦 Compare Sizing Models

For alternative methods: * Stock Buying: Sizing standard shares without premium decay. (See our Stock Options Sizing Guide). * Average True Range (ATR): Set stops based on price volatility rather than derivatives math. (See ATR Stop-Loss Sizing). * Use our client-side Position Size Calculator to quickly model share counts and risk targets.

Join the Urbandigistore Hub

Subscribe to receive premium developer cheat sheets, advanced conversion techniques, and campaign optimization checklists. Zero spam, unsubscribe anytime.