Stop-Loss Sizing: Position Sizing with Volatility-Adjusted Sharpe and Sortino Ratios

Compare Sharpe and Sortino ratios to optimize trading allocations by penalizing only downside volatility instead of overall variance.

🔧 Interactive Utility Tool

Try the free, 100% secure client-side tool associated with this guide. No registration required.

Position Sizing with Sharpe and Sortino Ratios

When designing a risk management system, quantitative traders use performance ratios to determine how much capital to allocate to different assets. While the Sharpe Ratio is the industry standard for evaluating risk-adjusted returns, it has a core limitation: it treats all price fluctuations (both upside runs and downside drops) as risk. To address this, advanced portfolio managers use the Sortino Ratio to size positions.

In this guide, we'll write out both formulas, compare standard deviation versus semi-variance, and outline trade sizing rules.

📐 Sharpe vs. Sortino: The Math Comparison

Both ratios evaluate excess return relative to volatility, but they define volatility differently:

1. The Sharpe Ratio Formula

The Sharpe ratio scales excess return against the total standard deviation ($\sigma_p$) of the asset's returns:

$$\text{Sharpe Ratio} = \frac{R_p - R_f}{\sigma_p}$$

2. The Sortino Ratio Formula

The Sortino ratio replaces standard deviation with downside deviation ($\sigma_d$, also known as semi-variance). It ignores positive returns and penalizes only negative returns that fall below a Target Acceptable Return ($T$):

$$\text{Sortino Ratio} = \frac{R_p - T}{\sigma_d}$$

$$\text{Where downside deviation } \sigma_d = \sqrt{\frac{1}{N} \sum_{i=1}^{N} \min(0, R_i - T)^2}$$

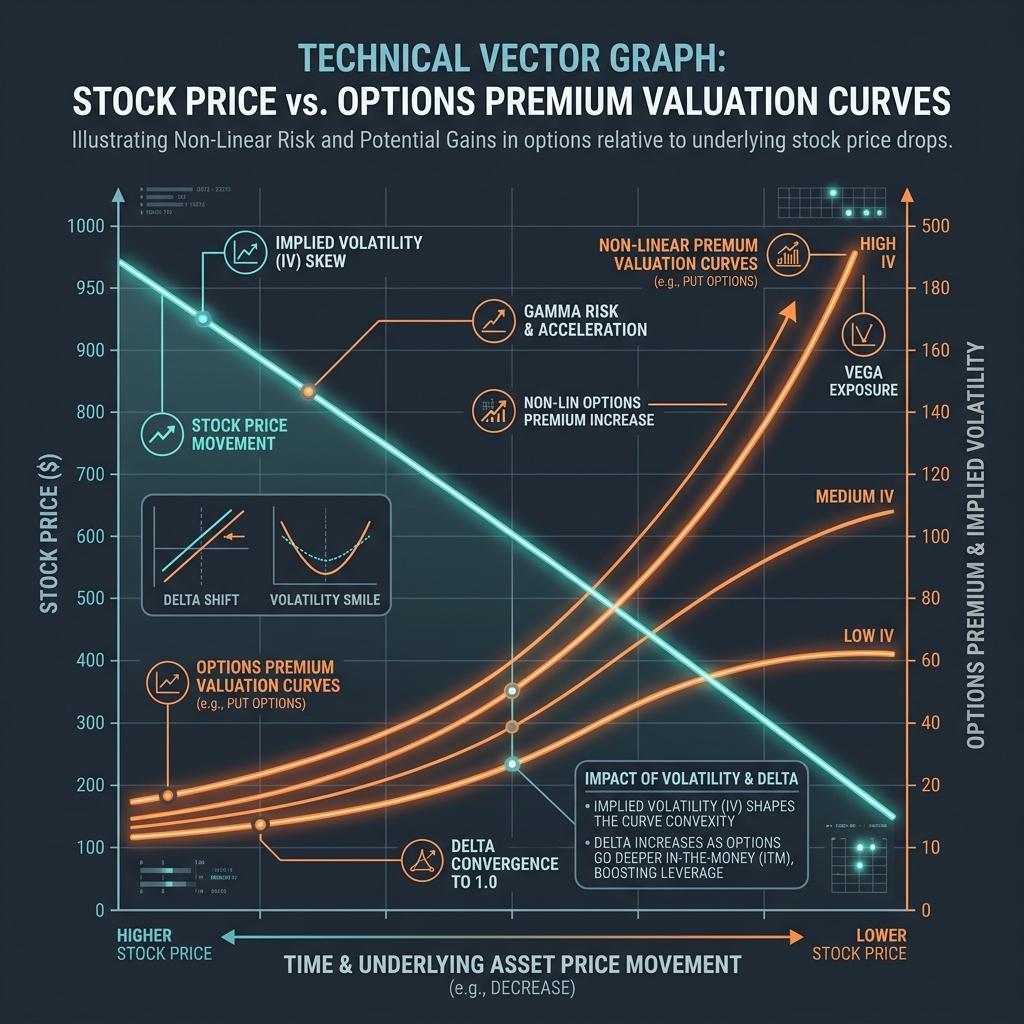

📊 Volatility Curves Reference

When trading options or volatile derivatives, risk exposure curves are non-linear. The chart below illustrates how option premium delta decay curves shift based on implied volatility (IV) and pricing boundaries:

🔍 Why the Sortino Ratio is Superior for Traders

Because the Sharpe ratio uses standard deviation, a strategy that experiences rapid, massive upward spikes will show a lower Sharpe ratio because those spikes increase the total variance. * The Flaw: Sharpe penalizes positive volatility, which is the exact outcome a trader wants. * The Solution: The Sortino ratio only penalizes downside volatility. A strategy with steady performance and sudden upward breakouts will have a significantly higher Sortino ratio, reflecting its true risk-adjusted superiority.

⚙️ Allocating Capital by Sortino Scaling

To maximize risk-adjusted equity growth: 1. Risk-Weight Allocations: Assign larger capital weights to assets displaying high Sortino ratios. 2. Scale Down High-Downside Assets: Assets with large downside semi-variance must receive smaller allocations, keeping your portfolio's total risk constant. 3. (See our Kelly Criterion Sizing Guide and Sharpe Ratio Sizing Guide to review mathematical formulas). 4. Compute Positions Instantly: Use our browser-based Position Size Calculator to quickly model share counts and risk targets.

Join the Urbandigistore Hub

Subscribe to receive premium developer cheat sheets, advanced conversion techniques, and campaign optimization checklists. Zero spam, unsubscribe anytime.

🚀 Launch Interactive Tool

Ready to test this directly? Open the secure web tool in a new sandbox tab.