Stop-Loss Sizing: Position Sizing by Volatility Index (VIX) Market Volatility

Learn how to scale stop-losses and position sizes using market-wide volatility indexes like the VIX to protect capital during market dumps.

🔧 Interactive Utility Tool

Try the free, 100% secure client-side tool associated with this guide. No registration required.

Position Sizing by Volatility Index (VIX) Market Risk

When trading individual stocks or crypto, it's easy to focus solely on the asset's own chart. However, when market-wide panic spikes, historical correlations break down, and almost all risk assets drop together. To protect your equity curve during these periods of high systemic risk, professional managers scale their position sizes and stop-loss boundaries based on broad volatility indexes like the CBOE Volatility Index (VIX).

In this guide, we'll explain what the VIX measures, detail volatility-scaling rules, and map risk limits.

📐 Understanding the VIX (The Fear Gauge)

The VIX measures the stock market's expectation of 30-day volatility implied by S&P 500 options pricing:

- VIX < 15: Indicates low systemic risk and high complacency. Ideal environment for standard swing trading.

- VIX 20 - 30: Indicates elevated market concern. Volatility is rising; price pullbacks are sharper.

- VIX > 30: Indicates extreme panic or capitulation. Assets correlate to 1.0, and price swings are massive.

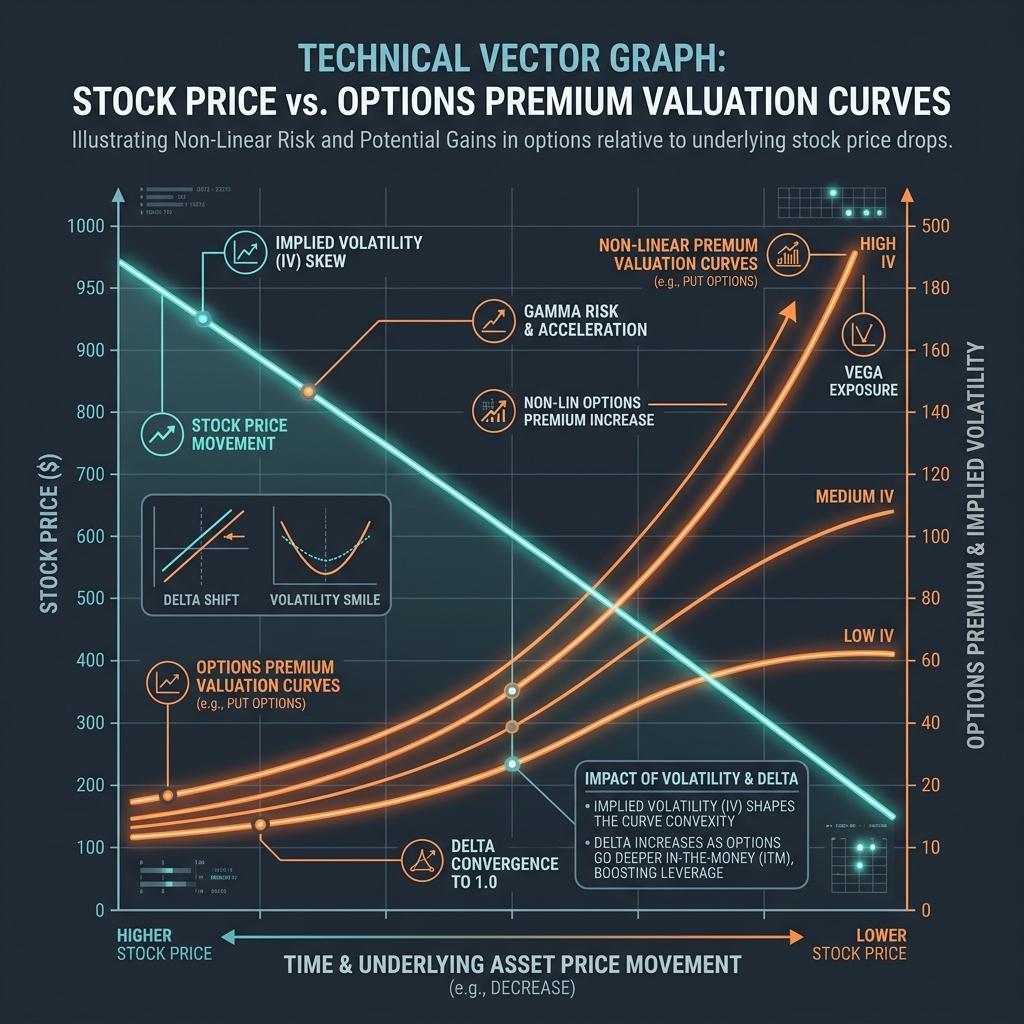

📊 Volatility Curves Reference

During market spikes, options premium delta decay curves shift rapidly, increasing risk for options buyers. The chart below illustrates how option premium delta decay curves behave across different implied volatility (IV) conditions:

🔍 The Volatility-Scaling Sizing Model

To protect capital, scale your risk per trade ($R_{\text{trade}}$) downward as the VIX increases:

| VIX Level | Systemic Risk | Stop-Loss Policy | Maximum Risk Per Trade |

|---|---|---|---|

| Below 15 | Complacent | Standard ATR Stops (2.0x ATR) | 2.0% of Account Capital |

| 15 to 25 | Elevated | Moderate Stops (2.5x ATR) | 1.0% of Account Capital |

| Above 25 | Extreme Panic | Tighten Stops & Halve Allocations | 0.5% of Account Capital |

This model ensures that when the overall market becomes unpredictable, you automatically trade smaller sizes. Even if a series of stop-outs occurs during a panic, your portfolio drawdown remains controlled.

🛠️ Portfolio Sizing Utilities

To structure your portfolio risk: * Structure Allocation Limits: Read Position Sizing with the Kelly Criterion to optimize wins. * Select Volatility Stops: Read Stop-Loss Multipliers Sizing Guide. * Compute Sizing Instantly: Use our browser-based Position Size Calculator to quickly model share counts and risk targets.

Join the Urbandigistore Hub

Subscribe to receive premium developer cheat sheets, advanced conversion techniques, and campaign optimization checklists. Zero spam, unsubscribe anytime.

🚀 Launch Interactive Tool

Ready to test this directly? Open the secure web tool in a new sandbox tab.